CONTENTS

Advisor Interest Is Real, but Early Stage

How Advisors Expect Private Markets to Enter DC Plans

Governance, Plan Suitability, and Fiduciary Context

Knowledge Gaps and Reliance on Institutional Support

Expected Demand from Plan Sponsors

Strategic Actions for Advisors and Committees

About The Retirement Advisor Council

Acknowledgements: Thanks to DCALTA (Defined Contribution Alternatives Association, its founder and President Jonathan R. Epstein AIF®, and Board Chair Michelle Rappa for their insightful contributions to this research

For additional information regarding this research, please contact:

Eric Henon

Executive Director

![]()

ehenon@retirementadvisor.us

+1.860.254.5042

Private market investments — long utilized by defined benefit plans, endowments, and foundations — are increasingly being evaluated within the defined contribution (DC) landscape. Structural shifts in public markets, heightened advisor familiarity, and the prospect of supportive regulatory guidance have elevated private equity, private credit, and real assets in retirement

plan discussions.

Advisors approach this evolution with measured interest. Unlike institutional pools with long dated liabilities, DC plans must consider participant liquidity needs, fiduciary obligations, and operational simplicity. As a result, adoption of private market assets is expected to be incremental and primarily channeled through professionally managed solutions rather than stand-alone menu options.

Advisor Interest Is Real, but Early Stage

Survey data confirms that private markets are transitioning from a theoretical topic to an area of active professional curiosity. However, most advisors describe adoption as being in the early innings, reflecting unresolved questions around liquidity, valuation, and fiduciary guidance.

Private market equity generates the highest level of interest, followed by private credit and real estate. Interest in more novel asset classes — such as commodities, infrastructure, or digital assets — declines meaningfully, suggesting advisors are more comfortable with familiar institutional strategies.

Interest in Alternative Asset Classes for Retirement Plans

Q1: The Executive Order issued in August ’25, regarding “alternative assets” mentioned several asset classes on which the DOL is to provide guidance. Of these, which would you be interested in evaluating for retirement plans? (check all that apply)

Advisors’ preferences skew toward private equity and debt, reinforcing that initial DC adoption will likely center on established asset classes rather than more experimental structures.i>

How Advisors Expect Private Markets to Enter DC Plans

Advisors overwhelmingly expect private markets to enter DC plans through professionally managed, multi asset structures. These solutions—most commonly off the shelf target date funds—allow fiduciaries to centralize liquidity management, valuation, and rebalancing at the fund level.

Stand-alone private market options are viewed as impractical for most plans in consideration of participant level liquidity needs and governance complexity. Managed structures also provide greater consistency in participant experience and simplify fiduciary oversight.

Expected Vehicles for Private Market Investments in DC Plans

Q2: How do you anticipate that private market investment products will be broadly available to Defined Contribution Plans at the close of the 2020s? (check all that apply)

Liquidity is a Major Concern

Liquidity emerged as the most frequently cited concern when advisors evaluate private markets for DC plans, followed by cost and fees, accurate investment risk measures and valuation/transparency. Cost and risk can only be assessed if an independent, generally accepted valuation is published daily. This hierarchy reflects the fiduciary reality that participants must be able to access their savings under normal and stressed market conditions.

Advisors emphasized that liquidity mechanics and valuation policies must be clearly documented and defensible, even in the event of potential Department of Labor safe harbor guidance. Appraisal based pricing, capital call timing, and smoothing effects remain areas of focus.

Top Considerations When Evaluating Private Markets for DC Plans

Q3: In your opinion, what factors should a plan sponsor or an advisor take into consideration as they explore the potential use of private market investment options in their plan? (Open-end)

| Theme | Tags |

| Liquidity | 42 |

| Cost/Fees | 26 |

| Risk (including fiduciary, concentration) | 22 |

| Transparency/Valuation | 15 |

| Participant Education/Communication | 14 |

| Manager Due Diligence | 11 |

| Benchmarking/Performance Evaluation | 9 |

| Portability | 7 |

| Regulatory/Fiduciary Consideration | 6 |

| Demographics/Participant Profile | 5 |

Governance, Plan Suitability,and Fiduciary Context

Not all DC plans are viewed as suitable candidates for private market exposure. Advisors consistently identified large plans with stable participant bases, sophisticated investment committees, and strong governance frameworks as the most viable starting point.

Smaller or resource constrained plans—particularly those with high turnover or limited participant financial literacy — are generally considered poor candidates until products and operational models further mature.

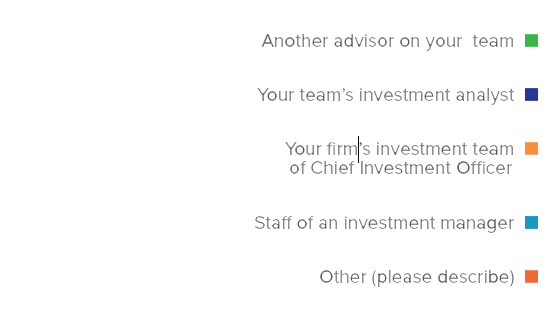

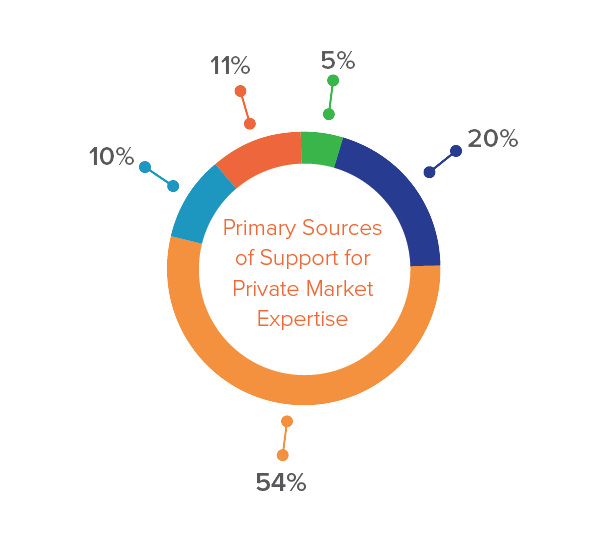

Knowledge Gaps and Reliance on Institutional Support

Despite growing interest, most advisors report only a working level understanding of private market investments. Advisors rely primarily on their firm’s investment teams or CIOs for guidance, rather than peers or external managers.

Q8: On whom do you rely foremost for help on private market products when needed?

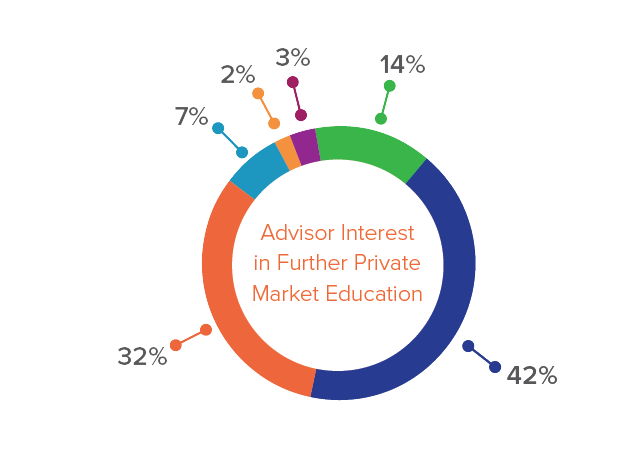

Educational demand is strong, with advisors expressing interest in webinars, conferences, and white papers that translate institutional concepts into DC appropriate frameworks.

Q18: What is your level of interest in learning more about private market investments to support discussions with plan sponsors?

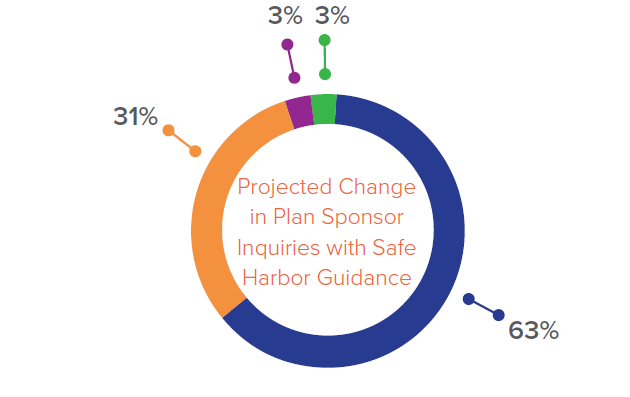

Expected Demand from Plan Sponsors

Looking ahead, advisors generally expect plan sponsor inquiries to increase modestly—though not dramatically—should the Department of Labor issue safe harbor guidance. This suggests that regulatory clarity may remove barriers but will not, on its own, trigger widespread adoption. Still, more than half (56%) of survey respondents said they are either “very interested in learning more” (42%) or “extremely interested and eager to engage” (14%), while another one-third said they are “somewhat interested and open to learning more.”

Q14: How do you anticipate that the number of plan sponsors who ask about private markets will evolve over the next 12 months, assuming the DOL formulates a safe harbor.

Strategic Actions for Advisors and Committees

As private markets continue their measured entry into DC plans, advisors and fiduciaries can prepare by taking these pragmatic steps:

- Focus on education to close internal knowledge gaps

- Include private markets within managed solutions, not as core menu stand-alone options

- Enhance transparency around liquidity, fees, and valuation

- Strengthen governance through IPS updates and committee education

- Monitor regulatory developments and align internal processes early

Conclusion

Private markets represent an evolutionary—not revolutionary—development in defined contribution investing. Advisors expect adoption to proceed gradually and primarily through professionally managed, multi asset vehicles that respect the liquidity and fiduciary demands unique to DC plans.

For well governed plans with appropriate scale, private markets may incrementally expand opportunity sets and diversify sources of return. Success, however, will depend far more on governance discipline and education than on regulatory changes alone.

About the Survey

This report is based on a survey of 69 retirement plan advisors who responded between 11/7/2025 and 12/6/2025. Respondents are members of the Retirement Advisor Council, a group of financial professionals who advise $1 trillion in plan assets. Among respondents, 49% work in teams with $3 billion+ in qualified retirement plan assets, 41% are affiliated with an RIA aggregator firm, 27% are independently owned, and 24% are affiliated with a NYSE firm.

Respondents operate across plan size segments: 47% target the under $3 million market; 85% target the $3 million to $29 million market; 85% target the $30 million to $99 million market, 73% target the $100 million to $999 million market; and 25% target the $1 billion+ market. A presentation of study results is posted Here.

This material is intended for an audience of financial advisors and ERISA plan fiduciaries residing in the United States. It is not intended for plan participants or for the general public.

The sole purpose of this material is to inform, and it in no way is intended to be an offer or solicitation to purchase or sell any security, other investment, or service, or to attract any funds or deposits. This article does not consider the actual or desired investment objectives, goals, strategies, guidelines, or factual circumstances of any investor in any fund(s). Before making any investment, each investor should carefully consider the risks associated with any investment, and make a determination based upon their own particular circumstances, that the investment is consistent with their investment objectives and risk tolerance.

Retirement plans are complex, and the federal and state laws or regulations on which they are based vary for each type of plan and are subject to change.

In addition, some products, investment vehicles, and services may not be available or appropriate in all workplace retirement plans.

Investments and concepts mentioned in this document may not be appropriate for all clients. Retirement plan sponsors and plan administrators should consult their investment, tax, and legal advisors and carefully consider all of the benefits, risks, and costs associated with a plan (a) before adopting any plan, (b) regarding any potential tax, ERISA and related consequences of any investments or other transactions made with respect to a retirement plan or account.

The Retirement Advisor Council does not sell securities, does not provide investment advice, legal advice, or tax advice. The Retirement Advisor Council is not an ERISA 3(16), 3(21), or 3(38) plan fiduciary.

About The Retirement Advisor Council

The Council advocates for successful qualified plan and participant retirement outcomes through the collaborative efforts of experienced, qualified retirement plan advisors, investment firms and asset managers, and defined contribution plan service providers.

Retirement Advisor Council is a brand of EACH Enterprise, LLC